Securing a personal loan hinges on understanding the approval process. The speed at which your application is processed can vary significantly, influenced by a multitude of factors ranging from your creditworthiness to the lender’s internal policies. This exploration delves into the intricacies of personal loan approvals, providing insights into what accelerates or hinders the process and equipping you with the knowledge to navigate it effectively.

We’ll examine the key elements impacting approval times, including your credit score, debt levels, the loan amount requested, and the type of lender you choose. We’ll also walk you through the application process step-by-step, highlighting crucial documentation and offering strategies to expedite the approval. Ultimately, our goal is to empower you with the understanding needed to secure your loan swiftly and confidently.

Factors Influencing Personal Loan Approval Speed

Securing a personal loan quickly hinges on several interconnected factors. Understanding these elements can significantly improve your chances of a swift approval. This section details the key influences on personal loan processing times, allowing you to better prepare your application and anticipate the timeline.

Credit Score’s Impact on Loan Approval Speed

Your credit score is arguably the most significant factor influencing loan approval speed. Lenders use credit scores to assess your creditworthiness – essentially, your ability to repay borrowed funds. A higher credit score (generally above 700) indicates a lower risk to the lender, leading to faster approvals. Conversely, a lower score may result in delays or even rejection, as lenders perceive a greater risk of default.

Specific credit score thresholds vary among lenders, but generally, higher scores unlock more favorable terms and faster processing times. For example, a borrower with a score of 750 might receive an instant approval for a smaller loan amount, while someone with a 600 score might face a more extensive review process, potentially involving manual underwriting and delays.

Debt-to-Income Ratio and Its Influence

The debt-to-income (DTI) ratio, calculated by dividing your monthly debt payments by your gross monthly income, is another crucial factor. A lower DTI ratio demonstrates your capacity to manage existing debt while taking on additional financial obligations. Lenders prefer applicants with lower DTI ratios, as it signals a reduced risk of default. A high DTI ratio can significantly slow down the approval process, as it indicates potential financial strain.

For instance, an applicant with a DTI ratio of 20% is more likely to receive faster approval than someone with a 50% DTI ratio, who might require further scrutiny.

Loan Amount’s Correlation with Approval Time

The amount of money you’re borrowing also affects approval speed. Smaller loan amounts generally involve less rigorous underwriting, leading to faster approvals. Larger loan amounts trigger more thorough reviews, increasing processing time as lenders need to carefully assess your ability to repay a substantial sum. For example, a loan of $5,000 may be approved much faster than a $50,000 loan, even if all other factors remain consistent.

Lender Policies and Their Impact on Approval Speed

Different lenders have varying approval processes and policies. Banks often have stricter underwriting criteria and longer processing times compared to online lenders. Credit unions, on the other hand, frequently offer more personalized service and potentially faster approvals for members, but their policies can also vary greatly. This is because each lender has different risk tolerance levels, internal procedures, and technological capabilities.

Comparison of Lender Approval Processes

| Factor | Banks | Credit Unions | Online Lenders |

|---|---|---|---|

| Approval Speed | Generally slower | Potentially faster for members; varies greatly | Often faster; can be instant for pre-qualified borrowers |

| Underwriting Process | Stricter, more thorough | More personalized, can be less stringent | Automated, often relies on algorithms |

| Documentation Requirements | Usually extensive | Can vary, often less extensive than banks | Generally less extensive, often digital |

| Interest Rates | Can vary; generally competitive | Often competitive, particularly for members | Can vary widely, often higher for higher-risk borrowers |

Income Verification and Employment History’s Role

Income verification and employment history are essential aspects of the loan approval process. Lenders require proof of consistent income to ensure you can afford the monthly payments. This typically involves providing pay stubs, tax returns, or bank statements. A stable employment history, demonstrating a consistent income stream over a reasonable period, significantly strengthens your application. Conversely, gaps in employment or inconsistent income can lead to delays or rejection.

Lenders often utilize third-party services to verify income and employment information, adding to the overall processing time. For example, a borrower with a consistent 5-year employment history and verifiable income will likely face a faster approval than a freelancer with inconsistent income streams.

The Loan Application Process

Applying for a personal loan can seem daunting, but understanding the process makes it much more manageable. This section provides a step-by-step guide to help you navigate the application journey, from initial inquiry to loan disbursement. Familiarizing yourself with each stage will increase your chances of a smooth and efficient application process.

Steps in the Personal Loan Application Process

The typical personal loan application process involves several key steps. Successfully completing each step is crucial for a timely approval. A thorough understanding of these steps empowers you to proactively address any potential issues.

- Initial Inquiry and Pre-Approval: You begin by contacting a lender (bank, credit union, or online lender) to inquire about personal loan options and potentially receive a pre-approval. This involves providing basic information about yourself and your desired loan amount. Pre-approval is not a guarantee of loan approval, but it provides an indication of your eligibility.

- Formal Application Submission: Once you’ve chosen a lender and loan product, you’ll need to complete a formal application. This usually involves filling out an online form or submitting a paper application, providing detailed personal and financial information.

- Documentation Submission: You will be required to submit supporting documentation to verify the information provided in your application. This is a crucial step, as lenders need to assess your creditworthiness and repayment ability.

- Credit Check and Underwriting: The lender will conduct a credit check to assess your credit history and score. Underwriting involves a thorough review of your application and supporting documentation to determine your eligibility for the loan and assess the risk involved.

- Loan Approval or Rejection: Based on the credit check and underwriting process, the lender will either approve or reject your loan application. If approved, you will receive a loan offer outlining the terms and conditions.

- Loan Agreement and Disbursement: If you accept the loan offer, you’ll need to sign a loan agreement. Once the agreement is signed, the lender will disburse the loan funds to your designated account.

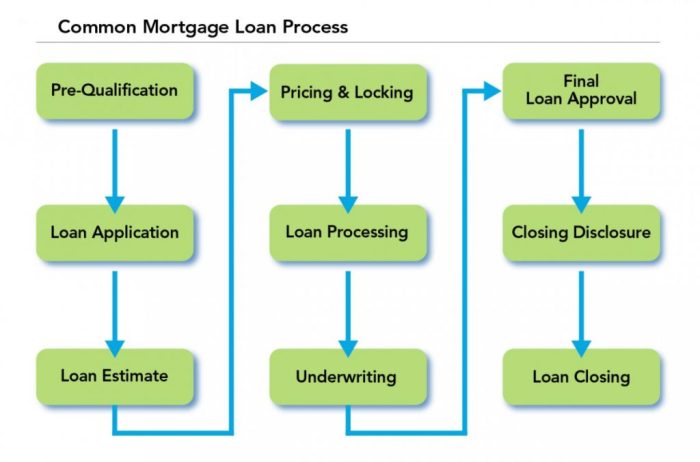

Flowchart of the Personal Loan Application Process

The following flowchart visually represents the various stages involved in a personal loan application:[Imagine a flowchart here. The boxes would be:

1. Initial Inquiry & Pre-Approval (Decision Point

Proceed or Not),

- Formal Application Submission,

- Documentation Submission (Documents listed below),

4. Credit Check & Underwriting (Decision Point

Approve or Reject),

5. Loan Approval/Rejection (Decision Point

Accept Offer or Decline), 6. Loan Agreement & Disbursement. Arrows connect each box, showing the flow of the process. Decision points are represented by diamonds.]

Required Documentation

Providing accurate and complete documentation is essential for a smooth and efficient application process. Missing or inaccurate documentation can lead to delays or rejection.

- Government-Issued Identification: (e.g., Driver’s License, Passport) Verifies your identity.

- Proof of Income: (e.g., Pay stubs, W-2 forms, tax returns) Demonstrates your ability to repay the loan.

- Proof of Address: (e.g., Utility bill, bank statement) Verifies your residency.

- Bank Statements: (e.g., Checking and savings account statements) Shows your financial activity and available funds.

- Employment Verification: (e.g., Letter from your employer) Confirms your employment status and income.

Understanding Loan Application Rejection Reasons

It’s disheartening to have a personal loan application rejected. Understanding the reasons behind the rejection is crucial for improving your chances of success in future applications. Lenders assess numerous factors before approving a loan, and a rejection doesn’t necessarily reflect negatively on your character or financial capabilities. It often points to areas needing improvement or clarification.Rejection reasons often stem from a combination of factors, not just one singular issue.

Therefore, addressing multiple aspects of your financial profile can significantly boost your approval prospects. Knowing what lenders look for and how to present your financial situation effectively can make all the difference.

Frequent Reasons for Personal Loan Application Rejection

Several common factors contribute to loan application rejections. These include low credit scores, insufficient income, high debt-to-income ratios, inconsistent employment history, and incomplete or inaccurate application information. Lenders use these factors to assess your creditworthiness – your ability to repay the loan as agreed. A strong credit history and stable financial situation are key indicators of this. Providing accurate and complete information is equally vital, as inaccuracies can raise red flags.

Strategies for Improving Approval Chances After Rejection

If your application is rejected, don’t be discouraged. Most lenders provide a reason for the rejection. Review this feedback carefully and identify areas for improvement. Improving your credit score is often the most significant step. This involves paying down existing debts, paying bills on time, and keeping credit utilization low.

Increasing your income or reducing your debt-to-income ratio are also beneficial steps. You can also re-apply after addressing the issues highlighted in the rejection notice, providing additional documentation to support your improved financial standing. Consider applying to lenders with less stringent requirements or exploring alternative loan options, such as secured loans or loans with co-signers.

Comparison of Rejection Reasons and Solutions

| Rejection Reason | Potential Solution | Example | Additional Considerations |

|---|---|---|---|

| Low Credit Score | Improve credit score by paying down debt, paying bills on time, and limiting new credit applications. | A score of 600 could be improved by consistently paying bills for 6-12 months, resulting in a score increase to 650-700. | Monitor credit reports regularly for errors and dispute them if found. |

| High Debt-to-Income Ratio | Reduce debt by paying down existing loans or consolidating debt. Increase income through a raise, second job, or side hustle. | Reducing credit card debt by $5,000 could significantly lower the debt-to-income ratio, increasing approval chances. | Budgeting and financial planning can help manage expenses and reduce debt. |

| Insufficient Income | Provide proof of additional income sources, such as rental income or investments. Secure a higher-paying job. | Providing documentation of part-time employment or freelance work can demonstrate increased earning potential. | Clearly demonstrate your ability to repay the loan despite the current income level. |

| Inconsistent Employment History | Highlight stable employment in your application. Provide detailed explanation for any gaps in employment. | Explaining a career change or a period of unemployment due to illness can mitigate concerns about job stability. | Emphasize skills and experience to showcase your employability and financial responsibility. |

| Incomplete or Inaccurate Application Information | Double-check all information before submitting the application. Provide all requested documentation. | Ensure accuracy of income, employment history, and contact information. | Seek professional assistance if needed to complete the application correctly. |

Accelerating the Personal Loan Approval Process

Securing a personal loan quickly often hinges on proactive steps taken by the borrower. Understanding the lender’s requirements and streamlining the application process are key to minimizing wait times. This section Artikels strategies to expedite loan approval, comparing different application methods and highlighting the importance of meticulous preparation.Applying for a personal loan can feel overwhelming, but a well-organized approach can significantly reduce processing time.

Careful planning and attention to detail can make the difference between a swift approval and a prolonged wait. This involves understanding the lender’s specific requirements, preparing all necessary documents in advance, and choosing the most efficient application method.

Online versus In-Person Application

Applying for a personal loan online offers several advantages over the traditional in-person method. Online applications are typically faster, more convenient, and often provide immediate feedback on application status. However, in-person applications can be beneficial for borrowers who prefer direct interaction with a loan officer and require personalized assistance navigating the process. The choice depends on individual preferences and circumstances.

Online applications usually allow for 24/7 access and quicker processing times due to automation. In-person applications, while potentially slower, offer the opportunity for immediate clarification of any questions or concerns.

The Impact of Thorough Documentation

Having all required documentation readily available significantly reduces processing time. Lenders require specific information to assess creditworthiness and risk. Delaying the process by requesting missing documents prolongs the approval timeline. Preparing documents such as proof of income, employment verification, and identification beforehand ensures a smooth and efficient application process. Examples of necessary documentation include pay stubs, tax returns, bank statements, and a valid government-issued ID.

The more complete and accurate the documents provided, the faster the lender can review the application. For example, if a lender requests three months of bank statements and the applicant only provides two, the process will be delayed until the missing statement is received.

Loan Application Best Practices

Applying for a personal loan can feel daunting, but by following best practices, you can significantly increase your chances of approval and streamline the process. Careful preparation and attention to detail are key to a successful application. This section Artikels strategies for accurate and efficient application completion, emphasizing the importance of honesty and thoroughness.Providing truthful and complete information on your personal loan application is paramount.

Lenders rely on the accuracy of this information to assess your creditworthiness and risk profile. Inaccurate or incomplete data can lead to delays, rejection, or even legal repercussions. Remember, lenders conduct thorough verification checks, and any discrepancies can severely damage your application. Transparency builds trust and increases the likelihood of a favorable outcome.

Importance of Accurate and Complete Information

Submitting a truthful and comprehensive application demonstrates responsibility and financial integrity. Lenders use the information provided to calculate your credit score, assess your debt-to-income ratio, and determine your repayment capacity. Omitting details or providing false information undermines this assessment, potentially leading to rejection. For example, failing to disclose existing debts could significantly impact the lender’s perception of your financial stability and ability to manage additional debt.

Similarly, providing inaccurate employment details can raise red flags and cast doubt on your ability to meet your repayment obligations. Complete and accurate information is crucial for a smooth and successful application process.

Common Mistakes to Avoid

Several common mistakes can hinder your personal loan application. Avoiding these errors will significantly improve your chances of approval.

- Inaccurate or Incomplete Financial Information: Providing incorrect income details, failing to list all debts, or omitting assets can lead to application rejection. Always double-check your figures and ensure all relevant financial information is accurately represented.

- Typos and Errors: Simple typos or errors in personal information, such as your address or date of birth, can create delays and confusion. Carefully review your application before submission.

- Poor Credit History: A poor credit history significantly reduces your chances of approval. Addressing any negative entries on your credit report before applying is crucial. Consider strategies for improving your credit score, such as paying down existing debts and maintaining good credit habits.

- Applying for Loans You Cannot Afford: Borrowing more than you can realistically repay can lead to financial difficulties. Carefully consider your monthly budget and repayment capacity before applying for a loan.

- Applying to Multiple Lenders Simultaneously: While shopping around for the best interest rates is wise, applying to numerous lenders in a short period can negatively impact your credit score. Space out your applications to avoid multiple hard inquiries.

- Ignoring Lender Requirements: Each lender has specific requirements. Failing to meet these criteria, such as minimum income thresholds or credit score requirements, will likely result in rejection. Carefully review the lender’s eligibility criteria before applying.

Post-Approval Procedures

Securing a personal loan is only half the battle; understanding the post-approval procedures is crucial for a smooth and successful borrowing experience. This section details the steps involved after your loan application is approved, from receiving the funds to managing your loan account effectively.The process typically begins with loan disbursement, followed by careful review of the loan agreement and adherence to the repayment schedule.

Understanding these aspects will help you avoid potential problems and maintain a positive credit history. This also includes proactively addressing any issues that might arise during the loan’s lifespan.

Loan Disbursement Methods

Loan disbursement, the process of receiving your approved loan amount, can occur through various methods. Common options include direct deposit into your bank account, a check mailed to your address, or transfer to a designated digital wallet. The chosen method will depend on the lender and your preferences, which are typically specified during the application process. For example, some lenders may prioritize direct deposit for faster and more secure transactions, while others may offer multiple options to cater to diverse customer needs.

Confirming the disbursement method and timeframe with your lender is vital to avoid delays or unexpected complications.

Understanding the Loan Agreement and Repayment Schedule

The loan agreement is a legally binding contract outlining the terms and conditions of your loan. It details the loan amount, interest rate, repayment schedule, fees, and other crucial information. Carefully reviewing this document before signing is paramount. The repayment schedule specifies the amount and due dates of your monthly payments. Understanding this schedule allows you to budget effectively and avoid late payments, which can negatively impact your credit score and incur additional fees.

For instance, a typical repayment schedule might involve fixed monthly installments over a specified period, such as 36 months or 60 months. Any deviation from the agreed-upon schedule should be discussed with the lender to avoid penalties or default.

Addressing Potential Post-Approval Issues

Even after approval, unforeseen circumstances can arise. These might include changes in your financial situation, difficulty making payments, or discrepancies in the loan documentation. Open communication with your lender is key to resolving such issues. For example, if you experience an unexpected job loss, contacting your lender immediately to discuss potential repayment options, such as a temporary deferral or a modified repayment plan, is crucial.

Ignoring these problems can lead to serious consequences, including damage to your credit score and potential legal action. Proactive communication and a willingness to collaborate with your lender can help navigate these challenges effectively.

Obtaining a personal loan quickly requires proactive preparation and a clear understanding of the approval process. By carefully considering the factors influencing approval speed, diligently gathering necessary documentation, and choosing the right lender, you can significantly increase your chances of a prompt and successful application. Remember, thorough preparation is key to navigating this process efficiently and securing the financial support you need in a timely manner.

Armed with this knowledge, you can approach your loan application with confidence and a clear path to success.

FAQ Guide

What is a good credit score for personal loan approval?

While requirements vary by lender, a credit score above 670 is generally considered favorable for securing a personal loan with competitive interest rates.

How long does income verification take?

Income verification times depend on the lender and the method used. It can range from a few days to several weeks.

Can I check my application status online?

Many lenders offer online portals to track application status. Check with your chosen lender for details.

What happens if my application is rejected?

Lenders typically provide a reason for rejection. Addressing the underlying issues (e.g., improving credit score, reducing debt) can improve your chances in future applications.

What’s the difference between a secured and unsecured personal loan?

Secured loans require collateral (like a car or savings account), often leading to faster approval but carrying risk of asset seizure if you default. Unsecured loans don’t require collateral, but usually have higher interest rates and stricter approval criteria.