Securing an auto loan can feel like navigating a complex maze, but understanding the process empowers you to make informed decisions. This guide demystifies the world of auto loan applications, from understanding the required information and navigating credit score impacts to selecting the right loan type and managing your debt responsibly. We’ll explore various application methods, compare lenders, and equip you with the knowledge to secure the best possible financing for your next vehicle.

Whether you’re a first-time buyer or refinancing an existing loan, this resource provides a structured approach to successfully completing your auto loan application. We will cover key aspects such as credit score influence, loan types, negotiation strategies, and responsible debt management, ensuring you’re well-prepared at each stage of the process.

Understanding Auto Loan Applications

Securing an auto loan involves completing an application, a crucial step in the car-buying process. Understanding the application process and the information required can significantly streamline the procedure and increase your chances of approval. This section details the typical components of an auto loan application, the information lenders require, and the different application methods available.

Auto loan applications typically gather comprehensive information about the applicant’s financial situation and creditworthiness to assess their ability to repay the loan. Lenders use this information to determine the loan amount, interest rate, and repayment terms they’re willing to offer. A thorough understanding of this process can empower you to navigate it effectively.

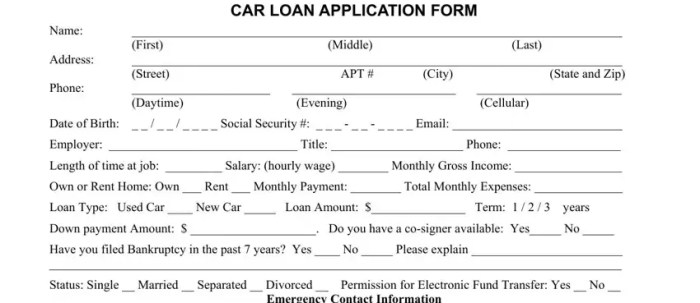

Typical Components of an Auto Loan Application Form

Auto loan applications usually request a range of personal and financial details. These commonly include personal identification information (name, address, date of birth, social security number), employment history (employer, income, length of employment), credit history information (allowing a credit check), details about the vehicle being purchased (make, model, year, VIN), and the desired loan terms (loan amount, loan term).

Some applications may also ask for additional information, such as assets, debts, and existing loans. Providing accurate and complete information is crucial for a smooth application process.

Information Required from Applicants for an Auto Loan

Lenders require a detailed picture of your financial standing to assess the risk involved in lending you money. This includes verifying your identity, assessing your income stability, and reviewing your credit history to determine your creditworthiness. They will also want details about the vehicle you intend to purchase and the loan terms you are seeking. The more transparent and accurate you are, the better your chances of securing favorable loan terms.

Different Types of Auto Loan Applications

Applicants can apply for auto loans through various channels, each offering a different level of convenience and interaction. Online applications, offered by many banks and credit unions, allow for a completely digital application process, often providing instant pre-approval. In-person applications, typically conducted at a dealership or bank branch, involve filling out a physical form and interacting directly with a loan officer.

Dealership financing often involves a streamlined process specific to the dealership’s lenders. Each method has its advantages and disadvantages depending on individual preferences and circumstances.

Comparison of Auto Loan Application Processes

The following table compares the application processes of three major lenders – a large national bank, a regional credit union, and an online lending platform. Note that specific processes and features can change, so it’s always best to check directly with the lender for the most up-to-date information.

| Lender Type | Application Method | Processing Time | Customer Service |

|---|---|---|---|

| Large National Bank | Online and In-Person | Typically 2-7 business days | Multiple channels (phone, online, branch) |

| Regional Credit Union | Primarily In-Person, some Online options | Potentially faster due to personalized service, but can vary | Usually strong emphasis on personalized service |

| Online Lending Platform | Entirely Online | Often faster, sometimes offering instant pre-approval | Primarily online chat and email support |

Credit Score Impact on Auto Loan Applications

Your credit score plays a pivotal role in the auto loan application process. Lenders use your credit history to assess your risk as a borrower. A strong credit history demonstrates your ability to manage debt responsibly, making you a more attractive borrower. Conversely, a poor credit history signals higher risk, potentially leading to loan denial or less favorable terms.Your credit score directly influences the interest rate you’ll receive on your auto loan.

Lenders categorize applicants into different risk tiers based on their credit scores, assigning higher interest rates to those deemed higher risk. This means a higher credit score typically translates to a lower interest rate, resulting in significant savings over the life of the loan. For example, a borrower with an excellent credit score (750 or above) might qualify for an interest rate of 4%, while a borrower with a fair credit score (600-650) might face an interest rate of 10% or more on the same loan.

This difference in interest rates can amount to thousands of dollars in extra interest paid over the loan term.

Credit Score Improvement Strategies

Improving your credit score before applying for an auto loan can significantly enhance your chances of approval and secure more favorable terms. This involves addressing any negative marks on your credit report and consistently demonstrating responsible credit management. Key strategies include paying all bills on time, keeping credit utilization low (ideally below 30% of your available credit), and maintaining a diverse credit mix.

Regularly checking your credit report for errors and disputing any inaccuracies is also crucial. Consistent and responsible financial behavior over several months can lead to a noticeable improvement in your credit score.

Financing Strategies for Applicants with Less-Than-Perfect Credit

Obtaining financing with less-than-perfect credit is challenging but not impossible. Several strategies can increase your chances of approval. One approach is to secure a co-signer with a strong credit history. A co-signer essentially guarantees the loan, reducing the lender’s risk. Another option is to explore loans from credit unions or smaller banks, which may be more lenient with applicants who have less-than-perfect credit.

Consider securing a smaller loan amount to reduce the lender’s perceived risk. Finally, building a positive payment history on smaller credit accounts, such as credit cards or installment loans, can gradually improve your credit score over time, making you a more attractive borrower in the future.

The Loan Application Process

Securing an auto loan involves a multi-step process that requires careful preparation and attention to detail. Understanding each stage will help you navigate the application smoothly and increase your chances of approval. This process typically begins with pre-qualification and ends with loan disbursement.

Steps in the Auto Loan Application Process

The application for an auto loan is a structured process, typically involving several key stages. A clear understanding of these steps will help you manage your expectations and prepare necessary documentation.

- Pre-qualification: Before formally applying, many lenders allow you to get a pre-qualification. This involves providing basic financial information to receive an estimated interest rate and loan amount you might qualify for. This helps you shop around and understand your borrowing power.

- Formal Application: Once you’ve chosen a lender and vehicle, you’ll complete a formal application. This typically involves providing detailed personal and financial information, including income, employment history, and credit history.

- Credit Check and Verification: The lender will pull your credit report and verify the information you’ve provided. This step is crucial for determining your creditworthiness and assessing the risk associated with lending you money.

- Loan Approval or Denial: Based on the credit check and verification, the lender will either approve or deny your application. If approved, you’ll receive a loan offer outlining the terms and conditions.

- Loan Documentation and Signing: If you accept the loan offer, you’ll need to sign the loan agreement and provide any remaining required documentation, such as proof of insurance.

- Loan Disbursement: Once all documentation is complete and verified, the lender will disburse the loan funds, usually directly to the car dealership.

Required Documentation for Auto Loan Applications

Gathering the necessary documents beforehand streamlines the application process. Having these documents readily available can significantly expedite the approval process.

- Proof of Income: Pay stubs, tax returns, or bank statements demonstrating consistent income.

- Proof of Identity: Driver’s license, passport, or other government-issued identification.

- Proof of Address: Utility bills, bank statements, or rental agreements showing current address.

- Credit Report: While the lender will typically pull your credit report, having a copy on hand can be helpful.

- Vehicle Information: Details about the vehicle you intend to purchase, including the make, model, year, and VIN (Vehicle Identification Number).

Negotiating Loan Terms and Interest Rates

Negotiating loan terms is a crucial step in securing a favorable auto loan. While lenders have set guidelines, there is often room for negotiation.Negotiating loan terms and interest rates often involves comparing offers from multiple lenders. For example, a borrower with excellent credit might negotiate a lower interest rate than someone with a less-than-perfect credit score. Factors such as the length of the loan term (e.g., 36 months vs.

72 months) also impact the overall cost of borrowing. A shorter loan term typically results in higher monthly payments but lower overall interest paid, while a longer term lowers monthly payments but increases the total interest paid. A borrower might negotiate a lower interest rate by offering a larger down payment or by choosing a shorter loan term.

It’s essential to shop around and compare offers before committing to a loan. Understanding your credit score and financial situation is key to successfully negotiating favorable terms.

Managing Auto Loan Debt

Successfully navigating an auto loan requires proactive management and a clear understanding of potential risks. Responsible handling of your loan minimizes financial strain and protects your creditworthiness. Failing to manage your loan effectively can lead to significant negative consequences.

Strategies for Responsible Auto Loan Management

Effective auto loan management involves consistent on-time payments, careful budgeting, and proactive communication with your lender. Prioritizing your loan payment ensures you avoid late fees and negative impacts on your credit score. Regularly reviewing your loan statement helps identify any discrepancies or potential issues. Open communication with your lender allows for addressing challenges before they escalate. For example, if you anticipate a temporary financial hardship, contacting your lender to explore options like forbearance or a payment plan can prevent default.

Consequences of Defaulting on an Auto Loan

Defaulting on an auto loan carries severe financial repercussions. Late payments negatively affect your credit score, making it harder to secure loans or credit cards in the future. Your lender may repossess your vehicle, leaving you without transportation and potentially facing additional fees and legal action. The repossession process can also impact your credit report significantly. Furthermore, defaulting on a loan can result in damage to your financial reputation, impacting your ability to rent an apartment or secure employment.

For instance, a significant drop in credit score can result in higher interest rates on future loans, increasing your overall borrowing costs.

Sample Budget Incorporating Auto Loan Payments

Creating a realistic budget is crucial for managing auto loan payments effectively. This example shows a monthly budget, adjusting it to your personal income and expenses.

| Income | Amount |

|---|---|

| Monthly Salary | $3000 |

| Expenses | Amount |

| Rent/Mortgage | $1000 |

| Groceries | $400 |

| Utilities | $200 |

| Auto Loan Payment | $350 |

| Gas | $150 |

| Insurance | $100 |

| Other Expenses | $400 |

| Savings | $400 |

This budget demonstrates how a $350 auto loan payment fits within a $3000 monthly income. Remember to adjust the amounts based on your individual circumstances. The key is to ensure your loan payment is consistently covered within your overall budget.

Tips for Avoiding Common Pitfalls Associated with Auto Loan Debt

Several strategies help avoid common auto loan pitfalls. Thoroughly researching and comparing loan offers from different lenders ensures you secure the best possible interest rate and terms. Understanding the total cost of the loan, including interest and fees, allows for informed decision-making. Avoiding unnecessary add-ons and carefully reading the loan contract prevents unexpected costs. Building an emergency fund provides a financial cushion to cover unexpected expenses and avoid loan default in times of financial hardship.

For example, having three to six months’ worth of living expenses saved can prevent a missed payment due to an unforeseen job loss or medical emergency.

Successfully navigating the auto loan application process requires careful planning and a thorough understanding of your financial situation. By understanding the various loan types, assessing your creditworthiness, and diligently completing the application, you can significantly increase your chances of securing favorable terms. Remember, responsible debt management is key to maintaining a healthy financial profile. This guide provides a foundation for a smooth and successful auto loan experience, enabling you to confidently drive off into the future.

Questions Often Asked

What happens if my auto loan application is denied?

A denial often indicates issues with your credit score or income. Review your credit report, address any errors, and consider improving your financial standing before reapplying. You might also explore alternative financing options.

How long does the auto loan application process typically take?

The timeframe varies depending on the lender and your individual circumstances. It can range from a few days to several weeks. Faster approvals are often associated with pre-approval and complete application packages.

Can I get an auto loan with bad credit?

Yes, but you may face higher interest rates and stricter requirements. Consider improving your credit score before applying or exploring lenders specializing in loans for individuals with less-than-perfect credit.

What is the difference between a secured and unsecured auto loan?

A secured loan uses the vehicle as collateral, typically resulting in lower interest rates. An unsecured loan doesn’t require collateral but usually comes with higher interest rates.