Securing a home loan is a significant financial undertaking, a journey filled with both excitement and potential complexities. Navigating the application process successfully requires understanding the various stages, from initial eligibility checks to the final closing. This guide provides a comprehensive overview, demystifying the process and empowering you to make informed decisions throughout.

From understanding your credit score and exploring different loan options to completing the application and navigating the underwriting process, we’ll cover all the crucial aspects. We’ll also offer practical tips and strategies to streamline the process and increase your chances of approval. Ultimately, this guide aims to equip you with the knowledge needed to confidently pursue your dream of homeownership.

Understanding the Home Loan Application Process

Securing a home loan can seem daunting, but understanding the process can significantly ease the journey. This section Artikels the typical steps involved, required documentation, and the various loan types available to help you navigate this important financial decision. Remember to always consult with a financial advisor for personalized guidance.

The Typical Steps Involved in a Home Loan Application

The home loan application process generally involves several key stages. A clear understanding of these steps will help you prepare effectively and manage your expectations.

- Pre-Approval: This initial step involves getting a pre-approval letter from a lender, outlining the maximum loan amount you qualify for. This strengthens your position when making offers on properties.

- Property Search and Selection: Once pre-approved, you can actively search for a suitable property within your budget.

- Loan Application: Submit a formal loan application to your chosen lender, providing all the necessary documentation.

- Loan Processing: The lender verifies your information, credit score, and the property’s value. This stage may involve appraisals and title searches.

- Loan Underwriting: The lender assesses your financial situation and the risk associated with lending you the money.

- Loan Closing: Once approved, you’ll sign all the necessary paperwork, and the funds are disbursed to complete the property purchase.

Required Documents for a Home Loan Application

Gathering the necessary documents beforehand significantly streamlines the application process. Below is a table outlining common documents required, categorized for clarity.

| Document Name | Description | Required or Optional | Where to Obtain |

|---|---|---|---|

| Application Form | The lender’s official application form, usually filled out online or in person. | Required | Lender’s website or branch |

| Proof of Identity | Passport, Driver’s License, or National ID card. | Required | Applicant |

| Proof of Income | Pay stubs, tax returns, bank statements (last 2-3 months). | Required | Employer, Tax Authority, Bank |

| Credit Report | A report detailing your credit history and score. | Required | Credit reporting agencies |

| Proof of Address | Utility bills, bank statements showing current address. | Required | Utility companies, Bank |

| Property Appraisal | Independent valuation of the property you intend to buy. | Required | Appraiser hired by the lender |

| Down Payment Proof | Bank statements, investment accounts showing funds for the down payment. | Required | Applicant’s Bank/Investment Accounts |

| Employment Verification | Letter from your employer confirming your employment and income. | Required | Employer |

Different Types of Home Loans Available

Several types of home loans cater to different financial situations and needs. Choosing the right loan depends on your individual circumstances and risk tolerance.

Common types include fixed-rate mortgages (offering consistent monthly payments), adjustable-rate mortgages (ARMs) where interest rates fluctuate, and government-backed loans like FHA and VA loans (often requiring lower down payments and more lenient credit requirements). Each loan type carries its own set of advantages and disadvantages, making careful consideration crucial.

Credit Score and Loan Eligibility

Your credit score is a crucial factor in determining your eligibility for a home loan. Lenders use it as a primary indicator of your creditworthiness and repayment ability. A higher credit score generally translates to better loan terms, including lower interest rates and potentially more favorable loan-to-value ratios. Understanding how your credit score impacts your loan application is essential for a successful home-buying experience.Lenders assess creditworthiness using a variety of factors, primarily centered around your credit history.

This involves reviewing your credit reports from agencies like Equifax, Experian, and TransUnion. These reports detail your past borrowing behavior, including payment history, amounts owed, length of credit history, and the types of credit you’ve used. Algorithms then convert this information into a numerical score, typically ranging from 300 to 850. The higher the score, the lower the perceived risk to the lender.

Factors Influencing Loan Eligibility Beyond Credit Score

While your credit score is paramount, other factors significantly influence your loan eligibility. These factors provide a more comprehensive picture of your financial stability and ability to manage a mortgage. Lenders carefully consider these elements alongside your credit score to make informed lending decisions.

- Debt-to-Income Ratio (DTI): This ratio compares your monthly debt payments (including the potential mortgage payment) to your gross monthly income. A lower DTI generally improves your chances of approval. For example, a DTI of 43% might be acceptable for some lenders, while others may prefer a DTI below 40%.

- Income and Employment Stability: Lenders want assurance of your ability to consistently make mortgage payments. A stable job history with consistent income demonstrates this reliability. Proof of income, such as pay stubs or tax returns, is often required.

- Down Payment Amount: A larger down payment reduces the lender’s risk, often leading to better loan terms. A substantial down payment can even help you qualify for a loan even if your credit score is slightly lower than ideal.

- Type of Loan: Different loan types have varying eligibility criteria. For example, FHA loans often have more lenient credit score requirements than conventional loans, but may require mortgage insurance.

- Assets and Savings: Demonstrating sufficient savings and liquid assets showcases financial responsibility and strengthens your application. These assets provide a buffer in case of unforeseen financial difficulties.

Strategies for Improving Credit Score

Improving your credit score before applying for a home loan can significantly increase your chances of approval and secure more favorable loan terms. Addressing the factors that negatively impact your credit score can yield substantial results over time.

- Pay Bills on Time: Payment history is the most significant factor in your credit score. Consistent on-time payments demonstrate financial responsibility.

- Reduce Credit Utilization: Keep your credit card balances low relative to your credit limits. High credit utilization indicates a higher level of debt and can negatively impact your score.

- Avoid Opening Multiple New Accounts: Applying for several new credit accounts in a short period can lower your score. Space out applications and only apply for credit when truly necessary.

- Address Negative Items on Your Credit Report: Review your credit report for any errors or inaccuracies. Dispute any negative items that are incorrect. If legitimate negative items exist, work towards improving your payment history.

- Consider Credit Counseling: If you’re struggling to manage your debt, consider seeking professional credit counseling. A credit counselor can help you create a budget and develop a plan to improve your financial situation.

The Loan Application Form and Process

Applying for a home loan can seem daunting, but understanding the application form and process can significantly ease the experience. This section will guide you through the typical steps, highlighting key information and potential pitfalls to avoid. A well-prepared application increases your chances of a quick and successful approval.

The application process generally involves completing a comprehensive form, providing supporting documentation, and undergoing a credit assessment. Lenders may vary slightly in their specific requirements, but the core elements remain consistent.

Sample Home Loan Application Form

The following is a representative example of the information typically requested in a home loan application. Note that the exact fields and requirements may vary depending on the lender.

- Personal Information: Full name, address, contact details, date of birth, social security number.

- Employment Information: Employer’s name and address, job title, length of employment, income details (pay stubs, tax returns).

- Financial Information: Current assets (savings, investments), liabilities (credit card debt, other loans), monthly expenses.

- Property Information: Address of the property, purchase price, down payment amount, estimated closing costs.

- Loan Details: Desired loan amount, loan term, interest rate type (fixed or adjustable).

- Credit History: Authorization to obtain a credit report.

Completing and Submitting the Application Form

Accuracy and completeness are paramount when filling out your home loan application. Take your time, double-check all information for errors, and ensure all required documents are attached. Many lenders offer online application portals, streamlining the submission process. Others may require paper applications mailed or delivered in person. Follow the lender’s specific instructions carefully.

Once completed, you will typically submit the application form along with supporting documentation such as pay stubs, bank statements, tax returns, and proof of down payment. The lender will then review your application and supporting documentation to assess your eligibility for a loan.

Common Mistakes to Avoid During the Application Process

Several common mistakes can delay or even derail your home loan application. Avoiding these errors can significantly improve your chances of a smooth and efficient process.

- Inaccurate Information: Providing false or misleading information is a serious offense and can lead to application rejection.

- Incomplete Application: Failing to provide all required documentation or information will delay the process.

- Ignoring Lender Requirements: Not following the lender’s specific instructions can lead to delays or rejection.

- Poor Credit Management: Applying for new credit during the application process can negatively impact your credit score.

- Insufficient Documentation: Failing to provide adequate proof of income, assets, and employment history can cause delays.

Tips for Ensuring a Smooth and Efficient Application Process

Preparing thoroughly and proactively can significantly streamline the home loan application process. These tips can help ensure a smoother experience.

- Review your credit report: Check for errors and take steps to improve your credit score before applying.

- Gather all necessary documentation: Organize your financial documents in advance to avoid delays.

- Shop around for the best rates: Compare offers from multiple lenders to find the most favorable terms.

- Read the fine print: Carefully review all loan documents before signing.

- Ask questions: Don’t hesitate to contact the lender if you have any questions or concerns.

Loan Processing and Underwriting

Once your home loan application is submitted, it enters the crucial phase of processing and underwriting. This involves a thorough review of your financial information to determine your eligibility for the loan and the associated risk for the lender. The process is rigorous and requires meticulous attention to detail.

The loan processing and underwriting stages are critical in determining whether your home loan application will be approved. These stages involve a detailed examination of your financial history, creditworthiness, and the property itself. The goal is to assess the risk associated with lending you money and ensure you have the ability to repay the loan.

The Role of the Underwriter

The underwriter is a key figure in this process. They act as the gatekeeper, evaluating the risk associated with your loan application. Their role encompasses a comprehensive review of your financial documents, including credit reports, income verification, employment history, and asset statements. They also assess the property’s value through an appraisal and verify the details provided in your application.

The underwriter’s decision ultimately determines whether you’ll be approved for the loan. They use a variety of criteria and models to assess the risk, and their judgment is based on the lender’s guidelines and regulations.

Steps Involved in Loan Processing and Underwriting

The loan processing and underwriting stages typically involve several sequential steps. These steps may vary slightly depending on the lender and the complexity of your application, but generally follow a similar pattern.

- Application Receipt and Initial Review: The lender receives your application and conducts an initial review to check for completeness and any obvious issues.

- Credit Report and Background Check: Your credit report is pulled, and a background check is performed to verify your identity and employment history.

- Income and Asset Verification: Your income and assets are verified through pay stubs, tax returns, bank statements, and other documentation.

- Property Appraisal: An independent appraiser assesses the value of the property you intend to purchase. This is crucial to ensure the property’s value justifies the loan amount.

- Loan Underwriting Review: The underwriter reviews all gathered information to assess your creditworthiness and the risk associated with the loan.

- Loan Approval or Denial: Based on the underwriting review, the lender decides whether to approve or deny your loan application. If approved, the terms and conditions are finalized.

- Closing and Funding: Once approved, the loan proceeds through closing, where all final documents are signed, and the funds are disbursed.

Potential Delays and Complications

Several factors can cause delays or complications during the loan processing and underwriting phase. Understanding these potential hurdles can help you prepare and manage expectations.

- Incomplete or Inaccurate Information: Missing or incorrect information on your application can lead to delays while the lender requests clarification or additional documentation.

- Credit Issues: A low credit score or recent credit problems can negatively impact your chances of approval or lead to higher interest rates.

- Income Instability: Recent job changes or inconsistent income can raise concerns about your ability to repay the loan.

- Property Appraisal Issues: If the appraised value of the property is lower than the purchase price, it can affect loan approval or require adjustments to the loan amount.

- Documentation Delays: Delays in obtaining necessary documents, such as tax returns or bank statements, can significantly prolong the process.

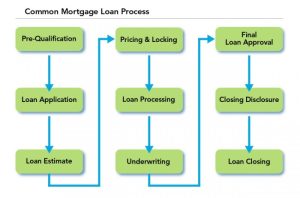

Loan Processing and Underwriting Flowchart

The following illustrates a simplified representation of the loan processing and underwriting stages.

Imagine a flowchart with boxes connected by arrows. The boxes would represent the following stages: Application Received -> Initial Review -> Credit & Background Check -> Income & Asset Verification -> Property Appraisal -> Underwriting Review -> Loan Approval/Denial -> Closing & Funding. The arrows indicate the progression from one stage to the next. This visual representation simplifies the process, highlighting the sequential nature of the steps involved.

Closing the Loan and Moving In

Successfully navigating the home loan application process culminates in the exciting final steps of closing the loan and moving into your new home. This phase involves several crucial procedures, from finalizing paperwork to transferring ownership and settling into your new property. Understanding these steps will ensure a smooth transition.

The closing process brings together all the parties involved in the home purchase – the buyer, seller, lender, and title company. It’s a significant milestone, marking the official transfer of ownership from the seller to you. This typically involves a final walkthrough of the property to verify its condition matches the agreement, reviewing and signing numerous documents, and the disbursement of funds.

The entire process can take several hours, so be prepared for a lengthy session.

Closing Costs

Closing costs are various fees and expenses associated with finalizing a home loan and purchasing a property. These charges are typically paid at closing and can significantly impact your overall financial outlay. While the exact amount varies depending on location and loan specifics, common closing costs include loan origination fees, appraisal fees, title insurance premiums, recording fees, and potentially prepaid property taxes and homeowner’s insurance.

It’s crucial to receive a detailed closing disclosure from your lender well in advance to understand these costs and budget accordingly. For example, a loan origination fee might be 1% of the loan amount, while title insurance could cost several hundred dollars. These fees are generally non-negotiable but are standard practice within the industry.

Property Ownership Transfer

The transfer of property ownership is a legally binding process handled through the title company. This company verifies the seller’s legal right to sell the property and ensures there are no outstanding liens or encumbrances. Once the loan is finalized and all conditions are met, the title company transfers the deed to the property into your name. This signifies the official change of ownership and is a critical step in completing the purchase.

The deed is a legally binding document that proves your ownership. The title company will typically record this deed with the local county recorder’s office, making the change of ownership a matter of public record.

Post-Closing Actions

After the closing is complete and you have the keys to your new home, several important actions should be taken to ensure a smooth transition and protect your investment.

It’s vital to take proactive steps to secure your new home and manage its upkeep. This includes changing the locks, scheduling home inspections (if applicable), and familiarizing yourself with the property’s systems and appliances. Furthermore, you should promptly notify relevant utility companies of your move and arrange for the transfer of services to your name.

- Change the locks on all exterior doors.

- Inspect all appliances and systems to ensure proper functionality.

- Notify utility companies of your move and arrange service transfers.

- Review your homeowner’s insurance policy and update your address.

- Register to vote at your new address.

Loan Application: A Broader Perspective

Securing a home loan is a significant financial undertaking, differing considerably from other loan types. Understanding these differences and embracing responsible borrowing practices are crucial for a successful and stress-free experience. This section compares and contrasts the home loan application process with other loan types, emphasizing the importance of responsible financial management and highlighting the consequences of neglecting loan terms.

The home loan application process is notably more extensive and rigorous than obtaining a personal or auto loan. This is due to the higher financial commitment involved and the longer repayment period. Home loans typically require a more thorough credit check, detailed financial documentation, and a comprehensive appraisal of the property being purchased. Personal loans, on the other hand, often involve a simpler application process with less stringent requirements, while auto loans fall somewhere in between, demanding a credit check and verification of income but generally less extensive documentation than a home loan.

Comparison of Loan Application Processes

The table below summarizes key differences in the application processes for home, personal, and auto loans.

| Feature | Home Loan | Personal Loan | Auto Loan |

|---|---|---|---|

| Credit Check | Extensive, including credit score and history | Moderate, focusing on credit score | Moderate, considering credit score and history |

| Income Verification | Thorough, requiring pay stubs, tax returns, etc. | Generally less stringent, often requiring only pay stubs | Requires income verification, often with pay stubs |

| Debt-to-Income Ratio (DTI) | Critically important, influencing loan approval | Important, but less stringent than for home loans | Important, but less stringent than for home loans |

| Collateral | The property being purchased | Usually unsecured | The vehicle being purchased |

| Application Process | Lengthy, involving multiple stages and documentation | Relatively short and straightforward | Moderately lengthy, requiring some documentation |

Responsible Borrowing and Financial Management

Responsible borrowing is paramount regardless of the loan type. It involves a thorough understanding of your financial situation, including income, expenses, existing debts, and credit score. Careful budgeting and planning are essential to ensure you can comfortably afford the monthly payments without jeopardizing your financial stability. A strong credit score significantly improves your chances of loan approval and secures you better interest rates.

Effective financial management, characterized by consistent budgeting, disciplined saving, and responsible debt management, directly impacts your loan application success. Lenders assess your financial history to gauge your repayment ability. A history of consistent on-time payments demonstrates financial responsibility, increasing your approval likelihood and potentially securing more favorable loan terms.

Consequences of Neglecting Loan Terms and Conditions

Ignoring loan terms and conditions can lead to severe financial consequences. Late payments result in penalties, impacting your credit score and potentially leading to loan default. Default can have serious repercussions, including damage to your credit rating, potential legal action, and repossession of collateral (in the case of secured loans like home or auto loans). Understanding and adhering to the terms, including payment schedules, interest rates, and any associated fees, is crucial for avoiding these negative outcomes.

For example, consistently missing mortgage payments can lead to foreclosure, resulting in the loss of your home. Similarly, failing to make timely payments on an auto loan can lead to repossession of the vehicle. These scenarios underscore the critical importance of responsible borrowing and meticulous adherence to loan agreements.

Successfully navigating the home loan application process requires careful planning, thorough preparation, and a clear understanding of the steps involved. By following the guidelines Artikeld in this guide, prospective homeowners can significantly improve their chances of securing a favorable loan and realizing their homeownership aspirations. Remember that proactive planning and attention to detail are key to a smooth and efficient process, ultimately leading to a successful outcome.

Questions Often Asked

What happens if my application is denied?

Lenders usually provide a reason for denial. Common reasons include low credit score, insufficient income, or high debt-to-income ratio. Review your application, address any issues, and consider reapplying after improving your financial standing.

How long does the entire process typically take?

The timeframe varies, but generally ranges from a few weeks to several months, depending on factors like loan complexity and lender processing times.

Can I get a home loan with bad credit?

While challenging, it’s not impossible. Lenders may offer loans with higher interest rates or stricter terms. Improving your credit score before applying significantly improves your chances.

What are closing costs, and how much should I expect to pay?

Closing costs cover various fees associated with finalizing the loan, such as appraisal fees, title insurance, and recording fees. These costs typically range from 2% to 5% of the loan amount but can vary.