Securing a mortgage is a significant financial undertaking, a pivotal step towards homeownership. This guide navigates the complexities of the mortgage loan application process, demystifying each stage from initial application to closing costs. Whether you’re a first-time homebuyer or a seasoned investor, understanding the intricacies of this process is crucial for a smooth and successful transaction. We’ll explore key aspects, including credit score impact, various loan types, and strategies to avoid common pitfalls.

From understanding the required documentation and navigating the pre-approval and underwriting phases to managing closing costs and post-approval responsibilities, this comprehensive guide offers a practical roadmap to achieving your homeownership dreams. We aim to empower you with the knowledge and confidence needed to make informed decisions throughout the entire mortgage application journey.

Understanding the Mortgage Loan Application Process

Securing a mortgage can seem daunting, but understanding the process can significantly reduce stress. This guide Artikels the typical steps involved, required documents, and provides a roadmap for first-time homebuyers. Navigating the application effectively hinges on preparation and a clear understanding of the expectations.

Typical Steps in a Mortgage Loan Application

The mortgage application process generally follows a series of sequential steps. These steps may vary slightly depending on the lender and the complexity of the loan, but the overall flow remains consistent. Delays can occur at any stage due to missing documentation or unforeseen circumstances.

Key Documents Required for a Mortgage Application

A complete mortgage application requires a comprehensive set of documents to verify your financial stability and the property’s value. Lenders need this information to assess your creditworthiness and the risk associated with lending you money. Failure to provide complete documentation will significantly delay the process.

- Proof of Income (pay stubs, W-2s, tax returns)

- Bank Statements (showing sufficient funds for down payment and closing costs)

- Credit Report (showing your credit history and score)

- Government-issued Photo Identification

- Property Appraisal (assessing the property’s value)

- Homeowners Insurance Quote

Step-by-Step Guide for First-Time Homebuyers

For first-time homebuyers, the process can feel overwhelming. This step-by-step guide simplifies the journey, offering a clear path towards securing your first mortgage. Remember to seek professional advice from a financial advisor or mortgage broker if needed.

- Pre-Approval: Get pre-approved for a mortgage to understand your borrowing capacity and strengthen your offer when making an offer on a home.

- Home Search: Begin searching for a home within your pre-approved budget. Consider factors like location, size, and features.

- Offer and Acceptance: Make an offer on your chosen home and negotiate the terms of the sale. Once accepted, you’ll proceed to the next stage.

- Loan Application: Complete and submit your mortgage application with all the necessary documents to your chosen lender.

- Underwriting: The lender will review your application, verify your information, and assess your risk.

- Closing: Once approved, you’ll attend the closing where you’ll sign all the necessary documents and receive the keys to your new home.

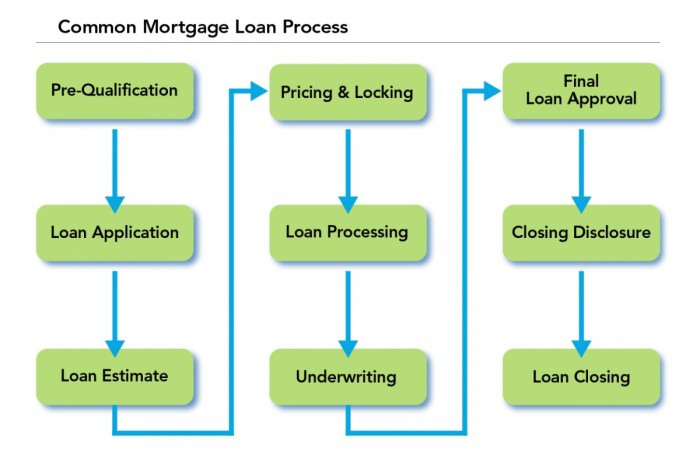

Flowchart Illustrating the Mortgage Application Process

Imagine a flowchart starting with “Initiate Application,” branching to “Gather Documents,” then to “Credit Check & Appraisal,” followed by “Loan Underwriting,” then “Loan Approval/Denial,” and finally “Closing.” A “No” decision at “Loan Approval/Denial” leads back to “Gather Documents” or “Address Issues” to rectify problems. A “Yes” decision leads to “Closing.”

Phases of the Mortgage Application Process

The mortgage application process can be logically divided into distinct phases, each with specific tasks. Understanding these phases helps manage expectations and track progress.

| Phase | Tasks | Timeline (Estimate) | Key Considerations |

|---|---|---|---|

| Pre-Application | Determine affordability, find a lender, pre-qualification/pre-approval | 1-4 weeks | Shop around for the best rates and terms. |

| Application | Complete application, provide documentation, credit check, appraisal | 2-6 weeks | Ensure all documents are accurate and complete. |

| Underwriting | Lender reviews application, verifies information, assesses risk | 4-8 weeks | Be responsive to lender requests for additional information. |

| Closing | Final paperwork, funding, property transfer | 1-2 weeks | Review all documents carefully before signing. |

Types of Mortgage Loans

Choosing the right mortgage is a crucial step in the home-buying process. Understanding the various types available, their features, and their suitability for different financial situations is essential for making an informed decision. This section will Artikel the key characteristics of several common mortgage loan types.

Several factors influence the type of mortgage that best suits an individual’s needs. These include credit score, down payment amount, income stability, and long-term financial goals. Each mortgage type presents a unique balance of risk and reward, impacting monthly payments, interest costs, and overall financial flexibility.

Fixed-Rate Mortgages

Fixed-rate mortgages offer predictable monthly payments throughout the loan term. The interest rate remains constant, providing borrowers with financial stability and allowing for easier budgeting. This predictability makes them a popular choice for those who prefer a consistent and reliable payment schedule. For example, a 30-year fixed-rate mortgage with a 4% interest rate will have the same monthly payment for the entire 30 years, barring any changes to property taxes or insurance premiums.

Adjustable-Rate Mortgages (ARMs)

Adjustable-rate mortgages feature interest rates that fluctuate over the life of the loan. The initial interest rate is typically lower than that of a fixed-rate mortgage, making them attractive to borrowers who plan to sell or refinance their home before the interest rate adjusts significantly. However, the risk lies in the potential for higher payments if interest rates rise.

For instance, an ARM might start with a 3% interest rate for the first five years, after which it adjusts annually based on market indices.

FHA Loans

FHA loans are insured by the Federal Housing Administration, making them accessible to borrowers with lower credit scores and smaller down payments than conventional loans typically require. This makes homeownership more attainable for a wider range of individuals. However, FHA loans often involve mortgage insurance premiums, adding to the overall cost. A borrower with a credit score slightly below the threshold for a conventional loan might find an FHA loan a viable option.

VA Loans

VA loans are backed by the Department of Veterans Affairs and are specifically designed for eligible veterans, active-duty military personnel, and their surviving spouses. These loans often require no down payment and offer competitive interest rates. However, eligibility is determined by military service and other specific criteria. A veteran returning from active duty could benefit significantly from the reduced financial barriers to homeownership provided by a VA loan.

Comparison of Mortgage Loan Types

| Mortgage Type | Interest Rate | Loan Term | Eligibility Requirements |

|---|---|---|---|

| Fixed-Rate | Fixed for the loan term | Typically 15 or 30 years | Good to excellent credit, sufficient income |

| Adjustable-Rate (ARM) | Adjusts periodically based on market indices | Typically 15 or 30 years | Good to excellent credit, sufficient income |

| FHA | Variable, generally higher than conventional loans | Typically 15 or 30 years | Lower credit score acceptable, lower down payment |

| VA | Variable, often competitive | Typically 15 or 30 years | Eligibility based on military service |

Loan Application Process

The mortgage loan application process can seem daunting, but understanding the key stages – pre-approval and underwriting – can significantly ease the journey. This section will clarify the procedures involved in each stage, highlighting the benefits and offering practical advice for a smoother experience.

Pre-Approval Process and its Benefits

Pre-approval involves a lender reviewing your financial information and providing a conditional commitment to lend you a specific amount for a mortgage. This isn’t a final approval, but it’s a strong indication of your borrowing power. The lender will assess your credit score, income, debts, and assets to determine your eligibility. This preliminary assessment offers several crucial advantages.

First, it gives you a clear picture of how much you can realistically borrow, enabling you to focus your house hunting on properties within your budget. Second, it strengthens your negotiating position when making an offer on a home; sellers often prefer buyers who are pre-approved because it signals a higher likelihood of a successful transaction. Finally, pre-approval can expedite the overall process once you find a suitable property, as much of the preliminary paperwork will already be complete.

Underwriting Process and Assessment Criteria

Underwriting is the rigorous process where a lender thoroughly evaluates your loan application to assess the risk involved in lending you money. Underwriters examine various factors to determine your creditworthiness and the likelihood of you repaying the loan. Key criteria include your credit history (including scores and payment patterns), debt-to-income ratio (DTI), employment history and stability, and the appraised value of the property you intend to purchase.

They’ll scrutinize your income documentation (pay stubs, tax returns), assets (bank statements, investment accounts), and liabilities (credit card balances, loans). A low DTI, a strong credit history, and stable employment significantly improve your chances of approval. The appraisal, which determines the property’s market value, is also critical; the lender will typically not lend more than a certain percentage of the appraised value.

Tips for Successfully Navigating the Underwriting Process

Preparing thoroughly for the underwriting process is crucial. Maintain accurate and readily accessible financial records. This includes pay stubs, bank statements, tax returns, and any other documentation that demonstrates your financial stability. Address any credit issues proactively; if you have blemishes on your credit report, work to improve your score before applying. Be upfront and honest with the lender about your financial situation; withholding information or attempting to misrepresent your circumstances can jeopardize your application.

Finally, be patient and responsive to the lender’s requests for additional information; delays in providing requested documentation can prolong the process.

Pre-Qualification versus Pre-Approval

Pre-qualification and pre-approval are often confused, but they are distinct processes. Pre-qualification is a less formal assessment based on information you provide to a lender. It typically involves a quick review of your financial details and provides a rough estimate of how much you might be able to borrow. It does not involve a formal credit check or verification of your income.

Pre-approval, on the other hand, is a much more thorough process involving a credit check, income verification, and a review of your overall financial profile. It results in a conditional commitment to lend, making it a far stronger indication of your borrowing capacity than pre-qualification. Choosing pre-approval over pre-qualification significantly strengthens your position when purchasing a home.

LOAN APPLICATION

Navigating the mortgage loan application process can be complex, and even minor errors can significantly impact your chances of approval or the terms you receive. Understanding common mistakes and how to avoid them is crucial for a smooth and successful application. This section highlights frequent pitfalls and provides strategies to ensure a strong application.

Common Application Errors and Their Consequences

Inaccurate or incomplete information is a primary cause of delays and rejections. For example, omitting a previous address or providing incorrect employment history can raise red flags and lead to further scrutiny, potentially delaying the process or resulting in denial. Similarly, underestimating your debt-to-income ratio (DTI) can significantly hinder your chances of approval, as lenders use this metric to assess your ability to repay the loan.

Failure to properly document income and assets also presents a major hurdle, as lenders require verifiable proof to confirm your financial stability. Finally, submitting a poorly prepared application with missing documentation or unclear information will likely result in delays and requests for additional paperwork.

Strategies for Avoiding Application Mistakes

Thorough preparation is key to a successful application. Before starting, gather all necessary documentation, including pay stubs, tax returns, bank statements, and identification. Carefully review each document for accuracy and completeness. Use a loan application checklist (provided below) to ensure nothing is overlooked. If you are unsure about any aspect of the application, seek professional guidance from a mortgage broker or financial advisor.

They can help you understand the requirements, gather the necessary documents, and ensure your application is accurate and complete. Taking your time and double-checking every detail will significantly reduce the risk of errors.

Application Checklist Before Submission

A comprehensive checklist is essential to prevent avoidable mistakes. Before submitting your application, ensure you have:

- Completed all sections of the application accurately and completely.

- Provided accurate and verifiable information regarding your income, employment history, and assets.

- Included all required supporting documentation, such as pay stubs, tax returns, and bank statements.

- Verified the accuracy of your debt-to-income ratio (DTI) calculation.

- Reviewed the entire application for any errors or omissions.

- Obtained pre-approval or pre-qualification to understand your borrowing capacity.

Successfully navigating the mortgage loan application process requires careful planning, meticulous preparation, and a clear understanding of the various stages involved. By diligently addressing each step, from improving your credit score to selecting the appropriate loan type and meticulously reviewing closing costs, you can significantly increase your chances of a successful application. Remember, proactive planning and attention to detail are key to securing your dream home.

Top FAQs

What is the difference between pre-qualification and pre-approval?

Pre-qualification is a preliminary assessment based on the information you provide; pre-approval involves a formal review of your credit and financial documents, resulting in a conditional loan commitment.

How long does the entire mortgage application process typically take?

The process can vary, but generally takes anywhere from 30 to 60 days, depending on factors like loan complexity and lender processing times.

Can I apply for a mortgage with a less-than-perfect credit score?

Yes, but a lower credit score may result in higher interest rates or stricter loan terms. Improving your credit score before applying is advisable.

What are some common reasons for mortgage loan applications to be denied?

Common reasons include insufficient income, poor credit history, high debt-to-income ratio, and inaccurate information on the application.

What happens after my mortgage loan application is approved?

After approval, you’ll proceed to closing, where you’ll sign the final loan documents, pay closing costs, and receive the keys to your new home.